When it comes to putting savings into something stable, many people in Singapore still turn to fixed deposits as a familiar and relatively low-risk option. While returns may not always be the highest compared to more aggressive investments, fixed deposits continue to attract attention for their simplicity, predictability, and peace of mind. This is especially true during periods when banks roll out limited-time promotional rates that are higher than usual.

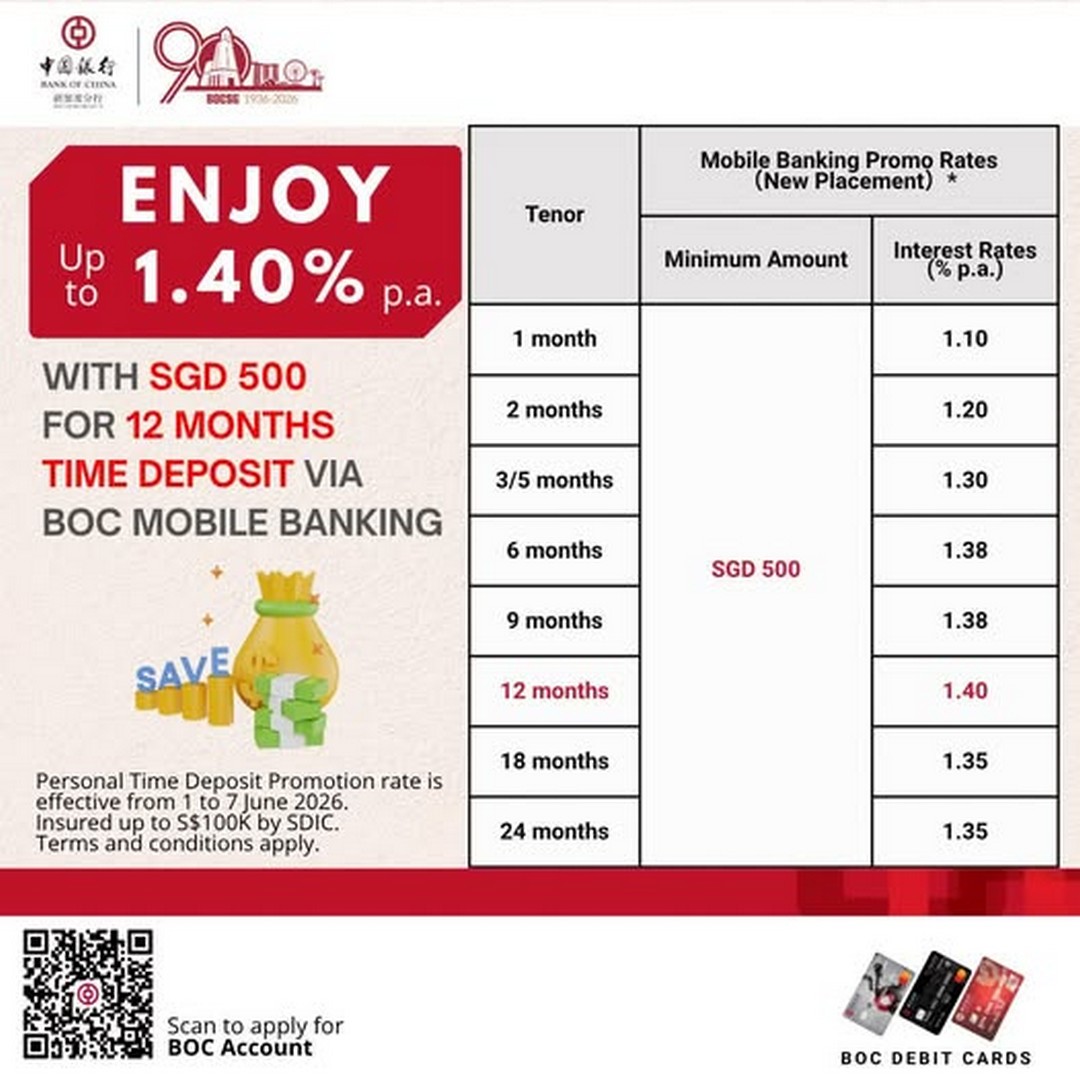

One such opportunity currently running is from Bank of China Singapore, offering a promotional fixed deposit rate of 1.40% per annum for a 12-month tenure, available through mobile banking placement. The promotion runs for a short window from 1 June to 7 June 2026, making it a time-sensitive option for those who have idle funds sitting in savings accounts.

This particular promotion is designed for individual deposit customers who prefer managing their finances digitally. With a minimum placement amount of S$500, it is relatively accessible compared to other financial products that often require higher entry amounts. The entire process is carried out via mobile banking, which means there is no need to visit a physical branch, fill out forms, or queue up during busy hours.

For many people juggling work, family commitments, and daily expenses, the convenience factor alone makes such digital fixed deposit placements appealing. Everything can be done in a few taps on a smartphone, and confirmation is usually instant. This ease of access is one of the reasons why banks continue to push digital-first promotions like this one.

Why this fixed deposit promotion stands out

In Singapore’s current financial environment, interest rates fluctuate depending on broader economic conditions, central bank policies, and global market movements. A rate of 1.40% p.a. for a 12-month fixed deposit may not sound extraordinary at first glance, but it becomes more meaningful when compared to standard savings account interest rates, which are often significantly lower unless bonus conditions are met.

For individuals who prioritise capital preservation over high-risk growth, locking funds into a fixed deposit can provide a structured way to earn passive interest. It is especially suitable for short-term savings goals such as building an emergency fund buffer, setting aside money for planned expenses, or simply parking cash that is not needed immediately.

Another important factor to consider is predictability. Once funds are placed into a fixed deposit, the interest rate is locked in for the duration of the tenure. This removes uncertainty and protects depositors from potential rate drops during the holding period. In an environment where financial markets can shift quickly, this stability can be a comforting feature.

Ease of mobile banking placement

The promotion is fully integrated into mobile banking, which reflects the ongoing shift in how banking services are delivered. Instead of relying on traditional branch-based processes, customers can now complete fixed deposit placements directly through their mobile devices.

This digital approach is particularly useful for individuals who prefer managing their finances independently. It allows them to compare rates, decide on placement amounts, and confirm transactions without needing assistance. The process is typically straightforward: log in to the mobile banking app, select the fixed deposit option, choose the promotional tenure, and confirm the placement.

For those who are already familiar with digital banking, this becomes a quick and seamless task. For others who are less experienced, the interface is usually designed to be intuitive, guiding users step-by-step through the process.

Limited-time opportunity

One of the key points that stands out in this promotion is its short validity period. Running only from 1 June to 7 June 2026, it is clearly designed as a limited-time campaign. This type of short promotional window is common in banking campaigns, as it encourages timely decision-making and helps customers take advantage of special rates before they revert to standard offerings.

Because of this limited availability, those who are considering placing funds into a fixed deposit may need to act quickly. Waiting too long could mean missing the promotional rate entirely, especially if funds are not readily available or if internal transfer processes take time.

Safety and deposit protection

Another important aspect of this promotion is security. Fixed deposits offered by established banks in Singapore are typically protected under the Singapore Deposit Insurance Corporation (SDIC), up to the applicable limit of S$100,000 per depositor per scheme member. This adds an additional layer of reassurance for individuals who are cautious about where they place their savings.

While fixed deposits are not designed for high returns, their appeal lies in security and stability. Combined with deposit insurance protection, they remain one of the more conservative financial tools available in the retail banking space.

Who may find this useful

This promotion may appeal to a variety of individuals. For example, those who have recently received bonuses or extra savings and are not ready to invest in higher-risk instruments may find this a suitable temporary parking option.

It may also be useful for individuals saving for short-term goals, such as upcoming travel, education expenses, or planned large purchases. Instead of leaving funds idle in a low-interest account, placing them into a fixed deposit for 12 months can help generate a modest return without requiring active management.

Even for more financially experienced individuals, fixed deposits can serve as part of a diversified portfolio, balancing out higher-risk investments with stable, low-volatility instruments.

Important considerations before placing funds

While the promotion offers a higher-than-standard rate, it is still important to consider liquidity. Once funds are placed into a fixed deposit, they are typically locked in for the full tenure. Early withdrawal, if allowed, may come with penalties or loss of interest.

It is therefore essential to ensure that the funds being placed are not needed for day-to-day expenses or emergency use. A common approach is to separate savings into different categories: liquid savings for immediate needs, and fixed deposits for medium-term parking.

Additionally, since rates are indicative and subject to change, the actual rate applied at the time of placement may differ slightly depending on the bank’s final terms. It is always advisable to confirm details during the transaction process.

Final thoughts

Overall, this fixed deposit promotion from Bank of China Singapore provides a straightforward and accessible way for individuals in Singapore to earn a stable return on their savings over a 12-month period. While it may not be the most aggressive wealth-building tool available, it serves an important role in financial planning by offering predictability and capital preservation.

For those who appreciate simplicity and want to make their idle funds work slightly harder without taking on unnecessary risk, this type of promotion can be worth considering. The combination of a competitive promotional rate, low entry requirement, and fully digital application process makes it a practical option for many everyday savers.

As with any financial decision, timing and suitability are key. With the promotional window only lasting a week, those interested may need to evaluate quickly whether this fits into their broader financial plans.

More details and official terms can be found at Bank of China Singapore.

Promotional/Event Details

Date: 1 June 2026 – 7 June 2026

Time: All day (via mobile banking)

Venue: Bank of China Mobile Banking App / Online Placement via Bank of China Singapore

Promotion: Fixed Deposit Promotion – 1.40% p.a. for 12-month tenure (minimum S$500 placement)

EverydayOnSales help brands connect with our community, the largest warehouse sales consumers database in Singapore. Advertise with EverydayOnSales Singapore.